"Liquidity" is the ability of some assets of a particular enterprise to quickly transform (transform) into other types of assets that are currently more in demand.

The most precise concept of “liquidity” is defined as a unit of time during which an asset is transformed, usually into cash.

Liquidity at the enterprise, in fact, shows its ability to cover its obligations. That is why they separate assets that are sold for a certain (average) period at a market price and assets for which the deadlines for execution are clearly indicated.

The liquidity of an enterprise, first of all, shows its ability to cover short-term liabilities for working capital. The liquidity ratio gives the most accurate and general idea of the liquidity of a company's assets. In order for the company to have a normal level of liquidity, necessary condition is the excess of the value of assets over the current amount of liabilities ("golden financial rule").

How to interpret meanings?

“Current liquidity ratio” (or as it is also called “general debt coverage ratio”) is an analytical indicator that is based on the calculation of the ratio between current assets and short-term (current) liabilities.

The current liquidity ratio shows how quickly and to what extent an enterprise can pay off its short-term debts (with a maturity of no more than one year). In this case, current assets with a certain market value act as a source of financing liabilities.

The higher the current liquidity indicator, the more stable the situation at the enterprise, since its solvency is higher. At the same time, experts mean not only the current solvency at a certain moment, but also the company's ability to pay its bills in the face of a sharp change in external financial circumstances that cannot be influenced.

The appearance of some force majeure may force the company's management to sell part of the reserves. This kind of activity is not the main profile of the company. The basis for calculating the current liquidity indicator is the company's balance sheet (accounting form number 1).

Having calculated the indicator of current liquidity, it is necessary to interpret it correctly.

Having calculated the indicator of current liquidity, it is necessary to interpret it correctly.

If the coefficient value is below 1.5, then this is a direct evidence that the company has some difficulties in covering its current liabilities.

However, this situation can be resolved by obtaining sufficient flow Money during the course of the company's operations. To do this, the expert needs to analyze the “Cash Flow Statement” (in form No. 4), line 4111. For example, for firms that are engaged in retail trade, this situation is quite acceptable.

An overestimated liquidity indicator often indicates insufficient use of working resources and limited access to short-term loans (including bank loans). For example, the accumulation of illiquid goods on a completely profitable company is characterized by a rapid increase in the current liquidity ratio.

Among other factors that may lead to an increase in the liquidity ratio, the following are distinguished:

- Tightening the terms of mutual settlements between suppliers and other counterparties.

- Excessive lending to buyers (when a company has a large amount of receivables, and there are practically no requirements for buyers regarding payment terms).

- Increase in stocks of raw materials and other materials in warehouses or in production.

At any enterprise, it is important to monitor the effectiveness of invested funds and evaluate the final result of the activity. For this, special calculations are carried out. and types of profitability (current assets, fixed assets, etc.).

Profit from sales is the end result of the company's activities. Here you will learn how to calculate profit and how you can increase the profitability of the enterprise.

Calculation formula

The calculation of the current liquidity ratio is carried out in accordance with this formula: K lt \u003d OK / TO,

- OK - the size of working resources (capital) of the company;

- TO - the amount of short-term obligations that must be paid by the company within one year from the date of their receipt.

Current liquidity ratio: balance sheet formula

The balance sheet of the enterprise serves as the basis for calculating the liquidity ratio. Absolutely all data is contained in the balance sheet.

- Where Кlt is the liquidity ratio (current).

- Line 1200 - the total of the company's working capital - raw materials, materials, cash (the sum of lines 1210, 1220, 1230, 1240, 1250 and 1260).

- Stock 1510 - borrowed resources; line 1520 - accounts payable.

- Line 1550 - other types of financial liabilities of the company.

- Lines 1510, 1520, 1550 are included in the fifth section of the balance sheet called "Current liabilities". This section also contains the line "Deferred income", however, its value is not taken into account in the calculation of liquidity.

To analyze the enterprise according to the balance sheet until 2011 ( old version), the following formula is applied: Klt \u003d line 290 / (line 610 + line 620 + line 630 + line 660),

- where Кlt – liquidity ratio (current);

- line 290 - the total of the company's working capital;

- stocks 610, 620, 630 and 660 are short-term financial liabilities of the company.

The formula for calculating the coefficient of the current level of liquidity can be written based on the degree of liquidity of the components of working capital, as well as the urgency of paying debts: K lt \u003d A k1 + A k2 + A k3 / (P a1 + P a2),

- where Кlt – liquidity ratio (current);

- And k1 - lines 1240 and 1250 - assets with a high level of liquidity;

- A k2 - medium liquid assets, line 1260;

- And k3 - assets with low level liquidity, lines 1210, 1220, 1230;

- P a1 - priority (urgent) obligations;

- P a2 - short-term loans (current liabilities), lines 1510 and 1550.

The higher the liquidity of working capital, the faster they can turn into money.

Standard value

Normative values of current liquidity ratios are determined based on guidelines for financial analysis companies.

Normative values of current liquidity ratios are determined based on guidelines for financial analysis companies.

The normal value of the liquidity ratio, which is accepted by most enterprises, lies in the range of 1.5-2.5.

The value of the coefficient less than one indicates problems with the timeliness of payment of the company's short-term debt (for the vast majority of companies). If we take a firm operating in the field of retail sales or catering, then the value of the coefficient equal to 1 will be considered normal, since these types of activities are characterized by a high level of short-term lending.

For industrial companies, the production cycle of which takes about a week, the normal value of the coefficient is considered to be 3, since these companies have a sufficient amount of inventory and work in progress.

Absolute liquidity ratio

Along with the current liquidity ratio, analysts use another indicator in their activities - the absolute liquidity ratio. What is it?

Along with the current liquidity ratio, analysts use another indicator in their activities - the absolute liquidity ratio. What is it?

The absolute liquidity ratio is financial instrument, which is equal to the ratio of cash and short-term investments of a financial nature that the company makes to short-term liabilities (the current level of liabilities).

The data for calculating the absolute liquidity ratio is the organization's balance sheet (according to accounting form №1).

Today there is a large number of application programs that allow you to quickly and easily calculate any coefficient and draw a conclusion about the company's activities.

The absolute liquidity ratio shows what percentage of short-term debts can be covered by the company's cash resources and their equivalents in the form of deposits, valuable papers or other highly liquid assets.

Calculations of the liquidity ratio are of interest not only to the company's management, but also to other (external) entities:

- investors who monitor current liquidity before investing;

- suppliers of raw materials and components who decide to grant a deferral of payment;

- bankers looking for short-term money back guarantees loan funds issued to the company.

The absolute liquidity ratio is calculated using the following formula: Klt =(cash resources + short term investments of a financial nature) / current level of liabilities.

In the foreign financial analysis of enterprises, a regulatory restriction is applied to the indicator of absolute liquidity. So, the normative limit Klt is 0.2. This means that every day the firm must be able to pay at least 20% of the amount of short-term financial obligations.

There is no exact justification for this standard value, however, most Russian companies"adopted" the calculation of the indicator of absolute liquidity. Thus, evidence of the normal activity of the enterprise is the fact that the amount of own funds should cover 20% of current (short-term) liabilities. However, for some domestic companies, taking into account the heterogeneity of the structure of short-term debt, the Klt indicator should be at least 0.5.

Labor intensity helps to determine the ratio of effort and time as accurately as possible. and specific index standards, read carefully.

Perhaps it will be useful for you: calculation of the average number of employees and penalties for failure to provide a document to the tax service.

Related video

In the article we will analyze the main solvency ratios of the enterprise and the formulas for their calculation.

The solvency of the enterprise. Definition

Solvency is the ability of an enterprise to repay its obligations to borrowers in a timely manner and in full. Solvency determines the financial condition, as a result, a decrease in the level of solvency leads to an increase in the risk of bankruptcy of the enterprise. To assess the financial condition, solvency ratios are used, which give a quantitative description of the enterprise.

To repay its obligations (credits), an enterprise can use both cash and different kinds assets that have varying degrees of liquidity. Thus, the solvency of the enterprise is formed due to two factors:

- availability of assets of the enterprise of various types;

- the level of liquidity of assets, which is determined by the degree of their realizability.

The structure of the company's assets

Consider the structure of the company's assets, which consists of current and permanent assets. Current assets of the enterprise- these are assets that can be converted into cash during one production cycle (1 year). Permanent assets consist of fixed assets of production, and are not directly involved in production. All assets of the enterprise are ranked according to the degree of liquidity, i.e. depending on the speed of their implementation (sales) and transformation into cash. The more an enterprise has highly liquid assets, the higher its solvency. Ranking of assets according to the degree of implementation speed:

Highly liquid liquid assets (A1)

Highly liquid assets enterprises form a group of current assets and have the maximum speed of implementation and their transformation into cash. The most liquid assets include: cash on hand, short-term financial investments in the bank and securities.

Marketable assets (A2)

Quickly realizable enterprise assets belong to the group of current assets and include receivables (<12 месяцев) и вклады в банк.

Slow selling assets (A3)

Slow selling assets are included in the group of current assets of the enterprise and include: accounts receivable (> 12 months), inventory finished products, raw materials and materials, work in progress and semi-finished products, VAT on acquired value.

Hard-to-sell assets (A4)

Hard-to-sell assets are permanent assets of the enterprise and include: buildings and structures, equipment, transport, land, intangible assets: patents, trademarks.

The difference between solvency and creditworthiness of the enterprise

The concept of solvency of the enterprise is closely related to creditworthiness. Let's take a closer look at their difference. The main difference is that solvency is the ability to repay your obligations with the help of any type of assets. Creditworthiness, on the other hand, reflects to a greater extent the repayment of obligations with the help of medium-term and short-term assets of the enterprise, excluding permanent assets: buildings, structures, vehicles, earth, etc. Repayment of obligations with the help of permanent and slowly realizable assets leads to a decrease in production capacity, and, consequently, a decrease in financial stability in the long term.

Solvency ratios of the enterprise

To assess the solvency of the enterprise, the following indicators are used:

Current liquidity ratio- reflects the ability of the enterprise to pay off its current obligations with the help of current assets. The calculation formula is as follows:

(analogue: urgent liquidity ) - shows the possibility of repayment with the help of quick-liquid and highly liquid assets of their short-term liabilities. The calculation formula is as follows:

Standard value for the quick liquidity ratio K bl >0.7-0.8.

Absolute liquidity ratio- reflects the ability of the enterprise with the help of highly liquid assets to pay off its short-term obligations. The indicator is calculated by the formula:

Standard value for K abl >0.2.

- shows the ability of the enterprise to pay off its obligations in full with all types of assets. This indicator includes not only short-term, but also long-term liabilities. The calculation formula is the ratio of the weighted sum of assets and liabilities.

If the overall liquidity ratio is K ol >1, the liquidity level is optimal.

The Law "On Insolvency (Bankruptcy)" identifies three coefficients that are used to assess the solvency of an enterprise: current liquidity ratio, solvency recovery ratio and solvency loss ratio. These indicators are currently used in practice as information indicators.

- reflects the company's ability to restore an acceptable level of current liquidity within 6 months. The formula for calculating the solvency recovery ratio is as follows:

K vp - coefficient of restoration of solvency of the enterprise;

The normative value of the indicator is considered to be Kvp>1 - reflects the ability of the enterprise to restore the level of solvency within 6 months. If K vp<1 – предприятие не располагает ресурсами для восстановления платежеспособности в течение 6-ти месяцев. К тому же, данный коэффициент строится на анализе тренда по двух периодам, что не является достаточно точным прогнозом динамики платежеспособности.

Loss of solvency ratio- reflects the possibility of deterioration in the solvency of the enterprise within 3 months. The formula for calculating this indicator is as follows:

To unitary enterprise - the coefficient of loss of solvency of the enterprise;

K tl - current liquidity ratio at the beginning (0) and at the end (1) of the reporting period;

K norms - the standard value of the current liquidity ratio (K norms = 2);

T is the analyzed reporting period.

Normative coefficient of loss of solvency K y > 1 - the degree of the threat of loss of solvency within 3 months is small. K pack< 1 – предприятие может потерять платежеспособность в течение 3-х месяцев. Коэффициент утраты платежеспособности аналогичен коэффициенту восстановления платежеспособности и показывает динамику изменения коэффициента текущей ликвидности предприятия по двум периодам. Это является его существенным недостатком, так как точность оценки направления тренда по двум данным низка.

Summary

In this article, we examined various solvency ratios of an enterprise and the formulas for calculating them. The company needs to quickly monitor the level of its solvency, as it directly determines its financial condition and sustainability of long-term development. In addition to liquidity ratios, solvency is affected by capital structure, profitability and turnover ratios, so an enterprise needs to have a system for assessing and diagnosing financial condition.

;

MZ - inventories;

KO - short-term liabilities (credits, loans and accounts payable). Or according to the formula: Ktl = TA / KO, where TA - current assets (2nd section of the balance sheet).

Based on the results of the calculation, set the standard value of this indicator, which should be at least 2.

The current liquidity ratio shows the payment capabilities of the enterprise, provided not only the repayment of receivables, but also the sale, if necessary, of tangible working capital.

If the balance sheet structure based on the calculation results is satisfactory, then in this case, calculate the solvency loss ratio for the next three months using the formula: Ktl at the end of the year + 3/12 * (Ktl at the end of the year - Ktl at the beginning of the year) / 2, where Ktl is the coefficient current liquidity;

3 - quarter (3 months);

12 - year (12 months).

The standard value must be at least 1.

note

The current liquidity ratio is determined from the consideration that the liquidity of the enterprise should be sufficient to meet short-term obligations.

Calculations must be made as of the beginning and end of the year to establish the standard value.

To pay off debts from the composition of working capital, it is really possible to use only finished products, receivables, excess inventories, cash, financial investments.

Sources:

- current liquidity ratio normative value

- Current liquidity ratio

The current ratio, also referred to as the coverage ratio, is used to determine how a company will respond to fleeting market changes. It is calculated based on data balance sheet during the reporting period. The analysis is made by comparison with indicators of previous periods.

You will need

- - balance sheet;

- - calculator.

Instruction

Determine the amount of the company's funds that are on the current account and on hand, as well as the value of securities, inventories and the amount of receivables. Sum these values and divide by the total amount of accounts payable, loans and credits of the company. The resulting value is the current liquidity ratio. To calculate it, you must first fill out the balance sheet in form No. 1.

Find the amount of current assets of the enterprise, which is necessary to calculate the current ratio. This value is determined on the basis of sections 1 and 2 of the balance sheet. Take the value of line 290 " current assets"And subtract from it the indicators of lines 220" Debt of the founders on contributions "and 230" Long-term receivables. If the last two values are absent, then the current assets of the enterprise are equal to the total in section 2 of the balance sheet.

Calculate the company's current short-term liabilities. To do this, you must completely fill out section 5 "Current liabilities" of the balance sheet and determine the total for it. Take the value of line 690 and subtract from it the value of lines 650 “Reserves for future expenses” and 640 “Deferred income”.

Calculate the ratio of current assets to current short-term liabilities to determine the current liquidity ratio. Analyze the resulting value to characterize the liquidity of the state of the enterprise. The higher the coverage ratio, the better the solvency of the company. The optimal value of this indicator is a value in the range from 1 to 3. If the coefficient is higher than 3, it is possible that the company is using capital irrationally. If below 1, then this indicates a high financial risk.

Related videos

To assess the financial reliability of an enterprise, it is necessary to carefully analyze the volume of its assets and liabilities. From their ratio, one can determine the current liquidity ratio, one of the three indicators of solvency.

You will need

- - balance sheet of the company.

Instruction

The calculation of the financial indicators of the liquidity of the enterprise allows you to assess its ability to repay current debts only through current assets. This allows you to objectively determine the possibility of financial risk in the unforeseen.

To determine the current liquidity ratio, you should use the formula: K \u003d (OA - DZ - Zuk) / TP, where: OA - current assets; DZ - accounts receivable; Zuk - debt of the founders for contributions to the company's capital; TP - current liabilities.

Take the data used to calculate this figure from the balance sheet. Current assets - line 290, which takes into account the fixed assets of labor (raw materials, materials, equipment with a service life of not more than a year, construction in progress at this stage, etc.)

Current assets go through three stages of the process, which ensures the continuity of the movement of capital. These are the monetary, production and again monetary stages. At the first stage, the invested money is converted into stocks of raw materials and starting materials, at the second - into finished products, and at the third - into cash proceeds.

Accounts receivable, line 230 of the balance sheet, is a set of debt claims of the enterprise. It includes amounts of money owed to the company by other companies and/or individuals. The debt of the founders for the contribution to the common capital is line 220.

Current liabilities - accounts payable of the enterprise. To calculate this value, take the difference between lines 690, 650 and 640. These are, respectively, total liabilities, reserves for future expenses and future income.

There are norms that the resulting value must comply with. If this indicator ranges from 1.5 to 2.5, then the company has stable financial capabilities. If the coefficient is below 1, then the company is exposed to a large financial risk. If it is more than 2.5, then this may be a consequence of the irrational use of capital.

Related videos

Tip 4: What are the differences between current and absolute liquidity

Liquidity is the ability of assets to be easily converted into cash. In a broad sense, liquidity is the solvency of an organization, i.e. her ability to meet her debts on time. To assess the solvency of the enterprise, indicators of absolute and current liquidity are calculated.

Current liquidity

In the process of assessing the liquidity and creditworthiness of the enterprise, the current liquidity indicator is calculated. This coefficient is calculated according to the balance sheet data and reflects the percentage of repayment of the firm's short-term liabilities by its current assets. The higher the debt coverage ratio, the more attractive the company for potential borrowers.

The current liquidity ratio is calculated by dividing the sum of all current assets by the amount of current liabilities. The value of current assets is determined by the indicators of the second section of the balance sheet "Current assets" and includes cash, stocks, liabilities of debtors, short-term financial investments. Current liabilities include short-term loans and borrowings accounts payable and the amount of other funds raised.

The normative value of the debt repayment ratio should be greater than 2. The calculation of this indicator is of particular interest to creditors, because its value reflects the ability of the enterprise to fully pay off its debts in the event of a decrease in the market price of assets.

Absolute liquidity ratio

It is calculated as the ratio of highly liquid assets to the value of the most urgent liabilities. As highly liquid assets, the amount of cash and short-term financial investments. Current liabilities are understood as short-term liabilities minus deferred income and reserves for future expenses.

From the calculation of the absolute liquidity ratio, it is possible to determine the amount of term liabilities that the organization can repay in as soon as possible. The optimal value of the coefficient is greater than 0.2. The value of this indicator is most important for future suppliers and short-term lenders.

Differences between current and absolute liquidity

The calculation of current and absolute liquidity ratios makes it possible to assess the solvency of the enterprise in the short term. Unlike the indicator of absolute liquidity, the coverage ratio reflects the ability of the enterprise to meet its debts in the long term.

Absolute liquidity shows the ability of the organization to repay its most urgent obligations with its own cash and collected receivables. When determining the indicator of current liquidity, not only money received from the sale of finished products and the sale of receivables, but also funds from the sale of current assets are taken into account.

For shareholders and potential investors, the indicator of current liquidity is of great importance, and for suppliers and creditors providing funds for a short period - the indicator of absolute liquidity.

Before investing money, the investor must decide for how long the investment will be made. And determine the ability to quickly get the money back on time. It is the liquidity indicator that reflects the ability to return the invested money on demand.

Investments help save money and protect them from inflation. The simplest method is Bank deposit. You can get money from the bank at any time. Therefore, we can say that a deposit in a bank belongs to highly liquid instruments.

A contribution to an unallocated metal account (OMA) allows you to make a profit on a change in the exchange rate precious metal. You can cash out the CHI account if necessary. However, you need to take into account the investment period and be sure that you will not need this money in the coming year. With an urgent withdrawal of funds, you can lose part of the capital due to the difference in the purchase price and the sale price.

It was profitable to invest in real estate at any time. In the long run, real estate is the most reliable investment. To return the money invested in square meters the property needs to be sold. This is where difficulties can arise. As a rule, for a quick sale, you will need to set the price slightly below the market. Much will depend on the location of the property. Therefore, the investment of money has low liquidity.

Stocks are among the most profitable and risky investments. Highly liquid shares are always in demand on the market and can be sold quickly and profitably. For low-liquid assets, the demand is lower and in case of an urgent sale, you can lose in price.

The liquidity of assets may vary depending on economic situation in the country and around the world. When choosing tools for increasing money, consider several financial indicators, then investments will bring good income and increase your capital.

Related videos

Any head of the enterprise knows the situation when there is a tense situation with the calculations (suppliers, taxes, loans, and so on). This means a solvency crisis. In order to avoid or minimize such situations, various calculated indicators are used, one of which is the solvency ratio. It is used as a current tool and for forecasting purposes.

The calculation is quite simple. In general terms, the overall solvency ratio:

Kp \u003d SK / (Ps + Pks + Pds)

Kp - payment coefficient;

SC - equity firms;

Ps - the most urgent liabilities (including overdue ones);

Pks - short-term liabilities (usually with maturities up to a year);

Pds - the volume of long-term liabilities (obligations for a period of one year or more, taking into account their repayment schedule).

Most often, Ps and Pks are not separated and are taken into account together.

Solvency ratio balance formula:

Kp \u003d (p. 1100 + p. 1200) / (p. 1400 + p. 1500)

The value of Kp obtained as a result of the calculation characterizes financial stability enterprises/firms.

If its value is higher than 0.5, then the situation is considered to be sufficiently stable and controlled. If this value is more than one, it means that the company's assets fully cover its liabilities and the position is very stable in the long term. Such values are typical for successfully operating industrial enterprises. With Kp less than 0.2, bankruptcy can occur at any time if urgent measures are not taken.

The given figures are not a dogma and organizations with a high capital turnover, especially in trade, successfully operate at Kp<0.5.

However, to get a complete picture of the current and general situation in the enterprise, other indicators should be taken into account.

Current solvency ratio

This value (Ktp) is the ratio of current assets (OA) to the amount of Ps + Pks:

Ktp \u003d OA / (Ps + Pks)

Read also: Offshore zones: what is it, a list

This coefficient should be considered in dynamics, since its value for a specific date is not informative or even distorts the picture.

Loss of solvency ratio

The value of this coefficient (Kup) is used in arbitration management and allows you to assess the ability of an enterprise to lose solvency:

Coup=0.5(Ctlik+3(Ctlik+Kntlik)/P)

Ktlik - current liquidity (coefficient) at the moment;

Kntlik - the value of Ktlik at the beginning of the analyzed period;

P - the analyzed period in months;

3 - the period of loss of solvency adopted in regulatory documents.

Meaning of Kup<1 означает высокую вероятность для предприятия потерять свою платежеспособность в течение трех месяцев.

Solvency recovery ratio

This indicator (Kvp) is calculated according to the following formula.

The company's solvency ratios act as indicators of its financial stability. They reflect the firm's ability to repay liabilities. A decrease in a number of indicators may indicate an approaching bankruptcy. Consider further what are the solvency ratios of the enterprise.

Formation features

The solvency of the enterprise is formed due to:

- The presence of assets. They can be presented in different forms.

- Degrees of liquidity of assets. It is determined by the level of realizability of funds.

The company's assets are divided into current and permanent. The first are those that can be turned into money during the production period (12 months). Fixed assets include fixed assets that are not involved in the direct release of goods. All assets are ranked by liquidity level. The analysis determines the speed of their sale and transformation into money. The more highly liquid assets a company has, the higher its solvency.

Funds classification

Depending on the speed of implementation, they are divided into:

Differences from creditworthiness

Solvency is closely related to this category. However, there is a significant difference between them. As mentioned above, solvency reflects the ability of an enterprise to repay obligations using any assets. According to creditworthiness, the state of repaying debts with the help of short- and medium-term funds is assessed. In this case, the analysis does not take into account fixed assets (structures, land, buildings, transport, etc.). If a company uses fixed and slow-moving funds to pay off liabilities, this can lead to a drop in production capacity. In the long term, this, in turn, will cause a decrease in financial stability.

Key indicators

The solvency of the enterprise is assessed by the following coefficients:

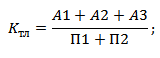

Current liquidity is Ktl>2. The optimal level is influenced by the industry affiliation of the company and the characteristics of its core business. This solvency ratio, therefore, must always be compared not only with the identified general normative indicators, but also with industry averages. The calculation is carried out as follows: Ktl \u003d (A1 + A2 + A3) / (P1 + P2).

Quick (term) liquidity

This solvency ratio reflects the company's ability to repay short-term liabilities through fast and highly liquid assets. The normative value for it is Kbl> 0.7-0.8. The calculation is carried out according to the formula: Kbl \u003d (A1 + A2) / (P1 + P2).

Absolute liquidity ratio

This solvency ratio illustrates a company's ability to repay its short-term debts using highly liquid assets. The optimal value of Cabl > 0.2. How is this solvency ratio calculated? The formula for it is as follows: Cable \u003d A1 / (P1 + P2)

General indicator

The overall solvency ratio on the balance sheet reflects the company's ability to fully repay obligations with all types of existing assets. This indicator includes not only short-term, but also long-term debts. The optimal level is Col>1.

Solvency recovery ratio

This indicator illustrates the possibility of returning the current liquidity to its normal value within six months from the reporting date. The value is determined by the ratio of the calculated level to the established one: Kvp \u003d [K1f + 6 / T (K1f - K1n)] / K1norm

- The actual value (at the end of the period) of current liquidity - K1f.

- Level at the beginning of the reporting period - К1н.

- Standard value - K1norm (equal to 2).

- Period of return of liquidity to the optimal value (in months) - 6.

- Reporting period (in months) - T.

If the solvency recovery ratio is greater than one when calculated for half a year, then this indicates that the company has the opportunity to return liquidity to the optimal level. If the value is less than 1, the situation for the company is unfavorable for the next three months from the reporting date.

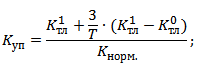

Loss of solvency ratio

It reflects the probability of a decrease in the value of the level of current liquidity to the established standard. The calculation is carried out as follows: Kup \u003d [K1f + 3 / T (K1f - K1n)] / K1norm.

If the solvency loss ratio is greater than one when calculated for a period of three months, then the company may not lose liquidity of assets in the near future. If the value is less than 1 for the same period, then the probability of loss is high.

Conclusion

The Law regulating the procedure and procedure for declaring insolvency (bankruptcy) identifies three main indicators that are used in assessing the solvency of a company:

- The level of current liquidity.

- Coefficients of recovery and loss of solvency.

Currently, these values are used in practice as information indicators. Nevertheless, when conducting a financial analysis in a company, all of the above elements are important. Only with their comprehensive study can a clear picture of the company's capabilities and the liquidity of its assets be formed. In this case, the calculation and analysis can be done for a specific time frame. Depending on the results, certain management decisions are made. In such cases, they will have a mathematical justification. In addition, calculations are also important for interested parties, including creditors.