Absolute liquidity ratio and indicator current liquidity serve as the main criteria for the IFTS assessing the solvency of a legal entity. Let's consider what these indicators are and what importance is attached to the first of them.

What does liquidity show?

The concept of liquidity is applied to the process of selling property owned by a legal entity. According to the speed of this implementation, it can be divided by the sold one:

- Almost instantly (money and short-term financial investments).

- Fast (short-term debt of debtors).

- After some time (stocks).

- Long (non-current assets).

With regard to the first three types of property that make up current assets, indicators are calculated to assess the ability of a legal entity to pay its short-term debts. These calculated characteristics are called liquidity ratios. There are three main types of them (depending on the speed with which property can be converted into money, which must ensure the repayment of existing debts): absolute, critical and current liquidity.

All these factors are used when analyzing the financial condition of a legal entity. Two of them (the first and the last) are obligatory for the calculation when assessing the paying capacity of a taxpayer, which is carried out by the Inspectorate of the Federal Tax Service according to the methodology contained in the order of the Ministry of Economic Development of the Russian Federation dated April 21, 2006 No. 104.

The absolute liquidity ratio, which will be discussed in our article, reflects what proportion of existing short-term debts can be repaid at the expense of the enterprise in as soon as possible, using for this the most easily realizable property.

Determine the initial data for calculating the absolute liquidity ratio for the balance sheet compiled for a specific reporting date, or for reporting for a number of dates, if you need to trace the dynamics of changes in this indicator.

How to calculate absolute liquidity?

The formula for the absolute liquidity ratio is a fraction, the numerator of which is the amount of easily realizable property, and the denominator is the amount of short-term debts. It can be presented in two forms, depending on what the denominator will be:

- Equal to the entire total amount for section V of the balance sheet (i.e., the total amount of short-term liabilities):

CLabs = (DenSr + KrFinVl) / KrObyaz,

KrFinVl - the amount of short-term financial investments;

Krobyaz - the total amount of short-term liabilities.

- Equal to the amount of actual debts (i.e., registered short-term debt on borrowed funds, as well as on ordinary debts to suppliers and other debts):

CLabs = (DenSr + KrFinVl) / (KrKr + KrCredZad + Prob),

КLabs - absolute liquidity ratio;

DenSr - amount Money;

KrFinVl - the amount of short-term financial investments;

KrKr - the amount of short-term borrowed funds;

KrKrZd - the amount of short-term debt to creditors;

Prob - the sum of other short-term liabilities.

In the second formula, the denominator can also be presented as the total amount of short-term liabilities, reduced by the amount of deferred income and estimated liabilities which are not real debts. If the last two amounts are significant, they can distort the meaning of calculating the coefficient. With such a change in the denominator, the formula will take on, accordingly, a different form, although the result will be the same as in the variant given by us in the conventional notation.

If, in both of the above calculations, the letter designations are replaced by the numbers of the corresponding lines of the balance sheet, then we will get the algorithms for determining the absolute liquidity ratio in the formulas for the balance:

- From the total amount of short-term liabilities:

CLabs = (1250 +1240) / 1500,

КLabs - absolute liquidity ratio;

1500 - the line number of the balance sheet with the total amount of short-term liabilities.

- From the amount of real debts:

CLabs = (1250 + 1240) / (1510 + 1520 + 1550),

КLabs - absolute liquidity ratio;

1250 - line number of the cash balance sheet;

1240 - line number of the balance sheet for financial investments;

1510 - line number of the balance sheet for short-term borrowed funds;

1520 - line number of the balance sheet for short-term debt to creditors;

1550 is the line number of the balance sheet for other short-term obligations.

The norm for the coefficient

The normal value of the coefficient is considered to be in the range from 0.2 to 0.5. This means that from 20 to 50% of short-term debts a legal entity is able to pay off in the shortest possible time at the first request of creditors. Accordingly, a higher value of the indicator indicates a higher solvency. An excess of 0.5 indicates unjustified delays in the use of highly liquid assets.

How to change the liquidity value?

An increase in the indicator is caused by an increase in the values indicated in the numerator of the calculation formula (money and short-term financial investments), and a decrease in the values that make up its denominator (short-term liabilities).

Absolute liquidity ratio(English analogue Cash Ratio) - the ratio of the most liquid part of assets and current (short-term) liabilities. The most liquid part of assets includes cash and cash equivalents. The indicator shows the share of the company's current liabilities that can be paid off immediately. This indicator belongs to the group of liquidity indicators.

Normative value

The value is considered normative from 0.1 to 0.2... A lower indicator indicates that the company will not be able to pay off debts on time if the payments are due soon. A value higher than the regulatory value can also indicate problems in the company and indicate an ineffective strategy for managing financial resources. Cash, unlike other assets, does not take part in the production and sales process, it does not generate income for the company. Therefore, a too high indicator indicates that a significant part of the capital is diverted to the formation of unproductive assets.

Directions for solving the problem of finding the indicator outside the regulatory limits

If the value of the indicator is below the standard, then the company can attract borrowed funds, implement some of the extra assets to increase the amount of the most liquid assets. If the value of the indicator is higher than the standard, then the company can invest part of the money(above the norm) in production and marketing activities, in financial investments, etc.

The formula for calculating the coefficient:

Absolute liquidity ratio = Cash and cash equivalents / Current liabilities

Notes and corrections

Cash is the means by which all participants in the financial process agree to exchange when making financial transactions. In order for cash to be classified as current assets, it is necessary that there are no restrictions on their storage and use. Such a situation is possible, for example, in the case of a court decision on the seizure of funds. If there are such restrictions, then it is necessary to adjust the indicator of cash and cash equivalents, which is used to calculate the indicator.

Companies often display restricted cash as cash and cash equivalents on the balance sheet. In this case, information on restrictions can be found in the notes to financial statements... In addition to reducing the amount of cash and cash equivalents by the amount of the limited portion, it is also necessary to adjust the value of current liabilities and deduct those associated with the restriction.

An example of calculating the absolute liquidity ratio:

Company OJSC "WebInnovation-plus"

Measurement unit: thousand rubles.

Absolute liquidity ratio (2016) = 75/242 = 0.31

Absolute liquidity ratio (2015) = 46/236 = 0.2

The data obtained show that in 2015 for each ruble of current liabilities there is about 0.2 ruble of cash and cash equivalents. Thus, the company OJSC "WebInnovatsiya-plus" could be responsible for its obligations in 2015. In 2016, the situation changed and the value of the coefficient was 0.31.

To reduce this value, it is advisable to direct part of the funds, for example, to purchase bonds of other companies. This will allow you to receive additional interest income and at the same time remain liquid. The optimal size of such an investment will be 75 - (242 * 0.2) = 26.6 thousand rubles. Accordingly, (75 - 26.6) = 48.4 thousand rubles. - this is the amount of cash and equivalents at which the absolute liquidity will be within the normative limits with the unchanged value of the amount of current liabilities.

The financial ratio received dividing cash and short-term financial investments into short-term liabilities... The data for the calculation is the company's balance sheet.

It is calculated in the FinEkAnaliz program in the Solvency Analysis block.

Absolute liquidity ratio - what it shows

Shows what proportion of short-term debt obligations will be covered by cash and cash equivalents in the form of market securities and deposits, i.e. absolutely liquid assets.

Liquidity ratios are of interest to the management of the enterprise and to external subjects of analysis:

- current liquidity ratio - for investors;

- absolute liquidity ratio- for suppliers of raw materials and supplies;

- quick liquidity ratio - for banks.

Absolute liquidity ratio - formula

General formula for calculating the coefficient:

Calculation formula according to the old balance sheet:

where p. 250, p. 260, p. 610, p. 620, p. 660- lines of the balance sheet (form No. 1)

A1 - the most liquid assets; P1 - the most urgent obligations; P2 - short-term liabilities

Calculation formula based on the new balance sheet data:

Absolute liquidity ratio - value

The regulatory limit K al> 0.2 means that at least 20% of the company's short-term liabilities are to be paid off every day. The specified regulatory restriction is applied in foreign practice. financial analysis... At the same time, there is no exact justification why, in order to maintain a normal level of liquidity of Russian companies, the amount of funds should cover 20% of current liabilities.

In Russian practice, there is a heterogeneity in the structure of current liabilities and maturity dates, so the normative value is insufficient. For Russian companies, the standard value of the absolute liquidity ratio is in the range of K al> 0.2-0.5.

Absolute liquidity ratio - scheme

Was this page helpful?

Synonyms

More found about the absolute liquidity ratio

- Influence of assets and liabilities turnover on the solvency of the organization M B Bellendir Absolute liquidity ratio ≥ 0.2 4, s 42-43 Fast liquidity ratio of strict liquidity 0.8-1.0 Coefficient

- Determining the balance sheet liquidity The most stringent liquidity criterion is the absolute liquidity ratio, which shows how much of the short-term debt the company can repay in the near future for

- Topical issues and modern experience in analyzing the financial condition of organizations - part 4 At the next stage, we will calculate the financial solvency ratios presented by the current quick and absolute liquidity ratios Current liquidity coverage ratio Ktl shows which part of current loan obligations and

- Influence of IFRS on the results of analysis of the financial position of PJSC Rostelecom IFRS from RAS - 1 Absolute liquidity ratio cash reserve ratio 0.20-0.25 0.811 0.074 -0.737 0.165 0.153 -0.012 2. Coefficient

- Balance sheet liquidity as one of the main areas of financial condition Balance sheet liquidity is determined using financial ratios- the absolute liquidity ratio is calculated as the ratio of the most liquid assets to the amount of the most urgent liabilities and

- Optimization of the balance sheet structure as a factor in increasing the financial stability of the organization Deviation of 2014 from 2012 - Absolute liquidity ratio not less than 0.15-0.20 0.334 0.529 0.020 -0.314 Adjusted liquidity ratio not less

- The relationship between financial risks and indicators of the financial position of the insurance company An increase in financial investments has reduced the total turnover, that is, market risks are also inversely related to the indicated indicator 5 Absolute liquidity ratio The absolute liquidity ratio was analyzed using the chain substitution method.

- Analysis of the financial condition in the dynamics of L9 x x x x 1.203 The absolute liquidity ratio shows what part of short-term liabilities can be repaid immediately and is calculated as

- Financial analysis of the company - part 4 In 2004, the liquidity ratio was 0.562, which means that the company is also not solvent and its short-term liabilities are much higher than current assets, but compared to 2003, the company's position has slightly improved. The absolute liquidity ratio shows what part of short-term debt the company can repay in the near future time This

- Features of financial analysis at agricultural enterprises Considering this fact, one can be taken as the criterion value of the overall liquidity indicator 2 The absolute liquidity ratio characterizes the company's ability to repay current short-term liabilities at the expense of cash

- Assessment of the influence of factoring and leasing on the indicators of the financial condition of transport companies This means that the amount of the company's equity capital is 44% of the total funding sources The absolute liquidity ratio is below the recommended value Only 13% of the total amount of short-term liabilities of the transport company

- Analysis of modern methods for identifying signs of deliberate bankruptcy Absolute liquidity ratio The absolute liquidity ratio shows what part of short-term liabilities can be repaid immediately and is calculated as

- The impact of estimated liabilities on liquidity indicators: problems and solutions of the FSFR RF, that is, this ratio is within the acceptable value The absolute liquidity ratio according to the enterprise was 0.2, which also fits into the acceptable standards However

- Topical issues and modern experience in analyzing the financial condition of organizations - part 8 Coefficients characterizing the debtor's solvency 2 Absolute liquidity ratio The absolute liquidity ratio shows what part of short-term liabilities can be repaid immediately

- Analysis of the FCD to identify signs of deliberate bankruptcy of CJSC Arsenal as of 01.01.2010 compared with the situation as of 01.01.2008 showed the following 1 The absolute liquidity ratio shows what part of short-term liabilities can be repaid immediately and is calculated as

- Analysis of the bankruptcy trustee EXAMPLE as of 01/01/2019 in comparison with the situation as of 01/01/2015 showed the following 1 The absolute liquidity ratio shows what part of short-term liabilities can be repaid immediately and is calculated as

- Forecasting bankruptcy of enterprises in the transport industry K7, where K1 is the absolute liquidity ratio K2 is the period of repayment of accounts receivable in KZ days.

- Financial ratios for financial recovery and bankruptcy For example, the absolute liquidity ratio is calculated as the ratio of the most liquid current assets to the current obligations of the debtor Here

- Features of the audit of the liquidity of the balance sheet of commercial organizations According to the balance sheet data to characterize the liquidity of an economic entity in economic literature it is recommended to count as a rule three relative indicators differing in the set of liquid assets considered as coverage of short-term liabilities absolute liquidity ratio intermediate coverage ratio current liquidity ratio When calculating all these indicators, use

- Cash liquidity ratio Synonyms absolute liquidity ratio The cash ratio is calculated in the FinEkAnaliz program in the Solvency Analysis block is shown by the formula

“Liquidity” is the ability of some assets of a certain enterprise to quickly transform (transform) into other types of assets that are currently more in demand.

The most accurate concept of "liquidity" is determined by the unit of time for which the asset is transformed, usually into cash.

The liquidity in the company, in fact, shows its ability to cover its obligations. That is why they distinguish between assets that are sold for a certain (average) period at the market price and assets for which the deadlines are clearly indicated.

The liquidity of an enterprise, first of all, shows its ability to cover short-term liabilities for working resources. The liquidity ratio gives the most accurate and general idea of the liquidity of a company's assets. In order for the company to have a normal level of liquidity, necessary condition consists in the excess of the value of assets over the current amount of liabilities ("golden financial rule").

How to interpret the meanings?

"Current liquidity ratio" (or as it is also called "total debt coverage ratio") is an analytical indicator that is based on calculating the ratio between current assets and short-term (current) liabilities.

The current liquidity ratio shows how quickly and to what extent an enterprise can pay off its short-term debts (with a maturity of no more than one year). The source of funding for liabilities in this case are current assets that have a certain market value.

The higher the indicator of current liquidity, the more stable the situation at the enterprise, since the higher its solvency. At the same time, experts mean not only the current solvency at a certain point, but also the company's ability to pay bills in the face of a sharp change in external financial circumstances that cannot be influenced.

The emergence of some kind of force majeure can force the company's management to sell part of the reserves. This kind of activity is not the main profile of the company. The basis for calculating the current liquidity indicator is the company's balance sheet ( accounting form number 1).

Having calculated the indicator of current liquidity, it is necessary to interpret it correctly.

Having calculated the indicator of current liquidity, it is necessary to interpret it correctly.

If the value of the coefficient is below 1.5, then this is direct evidence that the company has some difficulties in meeting its current liabilities.

However, this situation can be resolved by obtaining a sufficient cash flow in the course of the company's operating activities. To do this, the expert needs to analyze the "Statement of Cash Flows" (according to Form No. 4), line 4111. For example, for firms that are engaged in retail trade, this situation is quite acceptable.

A too high liquidity indicator often indicates insufficient use of working resources and limited access to short-term loans (including bank loans). For example, the accumulation of illiquid goods on a completely profitable company is characterized by a rapid increase in the current liquidity ratio.

Among other factors that may lead to an increase in the liquidity ratio, there are the following:

- Tightening of the terms of mutual settlements between suppliers and other counterparties.

- Excessive lending to buyers (when the company has a large amount of receivables, and there are practically no requirements for buyers regarding the timing of payments).

- Increase in stocks of raw materials and other materials in warehouses or in production.

Using the absolute liquidity ratio, they determine what part of immediate debts can be repaid using cash and their analogues ( valuable papers, bank deposits etc.). That is, through highly liquid assets.

The absolute liquidity ratio, along with other indicators of liquidity, is of interest not only to the management of the organization, but also to external subjects of analysis. So, this ratio is important for investors, quick liquidity - for banks; and absolute - to suppliers of raw materials and materials.

Definition and formula in Excel

Absolute liquidity shows the short-term solvency of the organization: whether the firm is able to pay off its obligations (with supplier counterparties) through the most liquid assets (money and their equivalents). The ratio is calculated as the ratio of funds to current liabilities.

The standard calculation formula looks like this:

Cubs. = (cash + short-term investments) / current liabilities

Cubs. = highly liquid assets / (most urgent liabilities + medium-term liabilities)

The data for calculating the indicator is taken from the balance sheet. Let's look at an example in Excel.

We have circled the lines that are needed to calculate the absolute liquidity ratio. Balance Formula:

Cubs. = (p. 1240 + p. 1250) / (p. 1520 + p. 1510).

Example of calculation in Excel:

We simply substitute the values of the corresponding cells into the formula (in the form of links).

Absolute liquidity ratio and standard value

The standard value of the coefficient accepted in foreign practice is> 0.2. The essence of the limitation: the enterprise must repay at least 20% of its current liabilities every day. Financial analysis practice in Russian companies adheres to the same principles. True, there is no justification for this approach.

The structure of short-term debt in Russian practice is heterogeneous. Maturities fluctuate significantly. Therefore, the figure 0.2 should be considered insufficient. For many enterprises, the rate of the coefficient is in the range of 0.2-0.5.

If the absolute liquidity ratio is below the norm:

- the company cannot immediately settle accounts with suppliers using cash of all types (including proceeds from the sale of securities);

- economists need to further analyze solvency.

A large increase in the absolute liquidity ratio shows:

- too many non-performing assets in the form of cash in cash and in bank accounts;

- additional analysis of the use of capital is needed.

Thus, the higher the indicator, the higher the company's liquidity. But excessively high values indicate an irrational use of funds: the company has an impressive amount of finance that is not "invested in business."

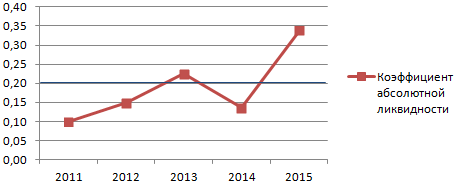

Let's go back to our example.

The values of absolute liquidity in 2013 and 2015 are within the normal range. And in 2014, the company experienced difficulties in paying off short-term liabilities.

Let us illustrate the dynamics of the indicator and display it on the chart for an illustrative example:

To make a complete analysis of the company's solvency, all indicators of the organization's liquid current assets are calculated. This ratio is used to calculate the share of short-term liabilities that can actually be repaid immediately. The example shows that the value for the period 2011-2015. increased by 0.24. In 2011, 2012 and 2014, the company experienced difficulties with paying capacity. But the situation has returned to normal - the company is able to fulfill its current obligations by 34%.