Is a receipt of an incoming cash order valid if half of the seal is put on it (that is, the second half fell on the side of the receipt note itself and was cut off when the receipt was issued to the buyer)? Will it be possible in a disputable situation in court to present such a document as proof of payment of the advance payment under the contract?

At its core, an incoming cash order is the primary document for accounting for cash at the cash desk of an organization, which indicates the information necessary for maintaining analytical accounting: from whom and on what basis the money was accepted.

The rules for processing primary documents from January 1, 2013 are regulated by Art. nine Federal law dated 06.12.2011 N 402-FZ "On accounting" (hereinafter - Law N 402-FZ). By this article, every fact of economic life is subject to registration by a primary accounting document.

By virtue of Part 4 of Art. 9 of Law N 402-FZ, the forms of primary accounting documents approve the economic entity upon the proposal of the official who is entrusted with maintaining accounting... Thus, from 01.01.2013, the forms of primary accounting documents contained in the albums of unified forms of primary accounting documentation are not mandatory for use. From that date, each organization (IP) independently develops and approves them in the accounting (clause 4 of PBU 1/2008 " Accounting policy organizations ").

However, there is an exception to this rule - the forms of documents used as primary accounting documents established by the authorized bodies in accordance with and on the basis of other federal laws continue to be mandatory for use (information from 04.12.2012 N PZ-10/2012). In particular, the forms of cash documents remain mandatory for use, since the use of unified forms of these documents is provided for by the regulatory legal acts of the Central Bank of the Russian Federation.

So, clause 5 of the Directive of the Bank of Russia dated March 11, 2014 N 3210-U "On the procedure for conducting cash transactions legal entities and the simplified procedure for conducting cash transactions and small businesses "(hereinafter referred to as Instruction N 3210-U), it is provided that the acceptance of cash by a legal entity, an individual entrepreneur is carried out according to cash receipts 0310001.

Thus, cash receipts (hereinafter also PKO) must be drawn up only in a unified form. The cash receipt form 0310001 (form No. KO-1) and instructions for its application and filling were approved by the decree of the State Statistics Committee of Russia dated 08/18/1998 No. 88 (hereinafter referred to as Instructions No. 88).

Clause 5.1 of Instruction N 3210-U, in particular, established that upon receipt of an incoming cash order 0310001, the cashier checks the presence of the signature of the chief accountant or accountant (if they are absent, the signature of the head) and its compliance with the sample, checks the correspondence of the amount of cash indicated in numbers , the amount of cash in words, the presence of supporting documents listed in the incoming cash order 0310001. If the deposited amount of cash corresponds to the amount specified in the incoming cash order 0310001, the cashier signs the incoming cash order 0310001, puts on the receipts to the incoming cash order 0310001, issued to the depositor of cash, an imprint of the seal (stamp) and gives him the specified receipt to the cash receipt order 0310001.

Instruction No. 88 also determined that a receipt for an incoming cash order is signed by the chief accountant or a person authorized to do so and by the cashier, certified by the cashier's seal (stamp) and registered in the register of incoming and outgoing cash documents (form No. KO-3) and issued into the hands of the person who handed over the money, and the cash receipt order remains at the cash desk. In the form N KO-1, props "M.P." it is also located on the receipt to the PKO.

Thus, from a direct reading of the given norms, we see that the seal is put on the receipt to the PKO, and not on the order itself. At the same time, these regulatory legal acts do not provide for the opportunity to put a seal print simultaneously on the PKO itself and the receipts to it (half of the print - on the PKO, the other half - on the receipt to the PKO).

Here, we note that the option of reflecting half of the seal imprint on any document, in principle, is not provided for by any regulatory legal act of the Russian Federation. The fact is that, according to the norms of the Civil Code of the Russian Federation, the seal is one of the means of individualizing a legal entity, that is, an object that individualizes and isolates a participant in civil legal relations. The seals must contain the full corporate name of the companies (JSC or LLC) in Russian and an indication of their location (clause 5 of article 2 of the Federal Law of 08.02.1998 N 14-FZ "On limited liability companies", p. . 7 article 2 of the Federal Law of 26.12.1995 N 208-FZ "On joint stock companies The seal imprint affixed on the document is not entirely (fragmentary) does not correspond to the main purpose of the seal - to individualize (reliably determine) a specific legal entity to which this seal belongs. simple language, displaying a seal on a document fragmentarily deprives the very procedure of certifying a document with a seal.

As it was said, the POC is the primary document. A specific, closed list of mandatory details of any primary accounting document is given in Part 2 of Art. 9 of Law N 402-FZ. Such a requisite as a seal imprint is not named in this list. This means that the affixing of the requisite in question on any primary document is optional. However, the PKO must be drawn up only in a unified form, and the unified form of the receipt to the PKO provides for the requisite "M.P.", in addition, the obligation to certify receipts to the PKO is directly established by Ordinance N 3210-U.

In this regard, we believe that the receipt to the PKO, certified by a fragment (half) of the seal, are primary documents drawn up in violation. This, in turn, entails various risks associated with the recognition of the legal force of such a document. For example, such negative consequences are possible as the refusal of the tax authority to recognize the receipt for the PQS with a half seal as a document confirming the taxable expenses of the organization, or the seller's refusal to recognize the receipt of cash. Money for the goods sold, etc. In such situations, the holder of this document will have to prove his case in court.

Of course, a receipt to the PKO, drawn up in violation: with a fragment of a seal or even without a seal at all, can be accepted by the court as evidence confirming the reality of the business transaction that has become the subject of the dispute. However, you need to understand that when considering a case, the courts consider the evidence presented by the parties in their totality and mutual connection. The presence of an incorrectly executed receipt to the PKO may serve as an additional argument in favor of confirming the correctness (or the plaintiff), but it will not be an unconditional proof that unambiguously testifies to the reality of the transaction.

Here are some examples of arbitration practice related to the incorrect reflection of the seal on a receipt to the PQS.

In the resolution of the Federal Antimonopoly Service of the Moscow District of July 30, 2009 N KA-A40 / 6945-09, the judges concluded that “the absence of numbers on individual receipts, the presence of one signature instead of two, the presence of a rectangular stamp instead of a round one, a readable print of half of the seal does not interfere tax control and do not indicate the absence of documentary evidence of expenses. "A similar conclusion was made in the decision of the Ninth Arbitration Court of Appeal dated 06.04.2009 N 09AP-3758/2009.

And in the ruling of the appellate ruling of the IC in civil cases of the court dated 04/10/2014 in case N 33-4373 / 2014, the judges, on the contrary, considered that the fragments of the round seal imprint on the receipts submitted by the defendant to cash receipts (the size of which on some receipts is less than half the size seals) do not allow them to be identified with the seal of JSC "...", in connection with which it is impossible to reliably establish that this evidence comes from this legal entity.

In the ruling of the Tenth Arbitration Court of Appeal dated December 17, 2013 N 10AP-11198/13, evaluating in aggregate all the evidence in the case file, taking into account "the indication in the receipt to the cash receipt order N 124 of July 31, 2012 and in the cash receipt order of various sales and purchase agreements; the absence of a fragment of the seal of JSC "I.T.I." T.I. "for July 2012 (cash book, register of incoming and outgoing cash documents), the Arbitration Court of Appeal concluded that the cash in the amount of 58 659 rubles 39 kopecks to the cash desk of CJSC" Enterprise "I.T. .AND." for the supply of information, technologists, engineering and equipment "from Evgeny Viktorovich Dashchenko under the contract of purchase and sale N 31/07/12 of July 31, 2012 actually did not arrive."

Similar conclusions were made by the court in the ruling of the Fourteenth Arbitration Court of Appeal dated 08/07/2014 N 14AP-3648/14: "in this case, the original receipt for the receipt cash order of Antares LLC dated 11/19/2012 does not contain the signatures of the chief accountant and cashier of Antares LLC" , and the fragment of the seal imprint on this document does not allow us to make a reliable conclusion about its belonging to LLC "Antares" ... Under the above circumstances, the conclusion of the court of first instance that the said document does not confirm the fact that the defendant paid money to the plaintiff's cashier seems to be correct " ...

At the same time, in the decision of the Eleventh Arbitration Court of Appeal dated 15.10.2014 N 11AP-13111/14, the court rejected the arguments of the appeal about the absence, in particular, of a seal in cash receipts due to the fact that such a requisite as a seal is not mandatory the requisite of the primary accounting document, since in Part 2 of Art. 9 of Law N 402-FZ, this requisite is not named.

In conclusion, we note that, indeed, at present there is an opinion that, based on the customs of business, one seal is put on an incoming cash order and a receipt for it in such a way that part of the seal is on the incoming cash order, and part is on the receipt for the receipt. cash order, then the receipt is torn off and issued to the person who deposited the funds. This opinion is also taken into account by the courts when making a decision, but the court still considers all the evidence in conjunction with each other. For example, see the resolution of the Eighth Arbitration Court of Appeal dated July 30, 2014 N 08AP-5256/14, the resolution of the Fourteenth Arbitration Court of Appeal dated August 27, 2012 N 14AP-5527/12.

Moreover, we came across an example of arbitration practice - an order Arbitration court from 18.12.2009 in case N А03-6686 / 2009, where the court did not consider (rejected) the receipts to the PKO and copies of the PKO, which he referred to in support of the debtor's monetary obligation, as evidence, due to the absence of the second half of the organization's seal on the copies of the PKO. We note that, in our opinion, such an opinion is erroneous, we draw your attention to the fact that subsequently the indicated conclusion of the judges of the Arbitration Court of the Altai Territory was recognized by the appellate court as inconsistent with the factual circumstances and the available evidence (resolution of the Seventh Arbitration Court of Appeal dated 06.04.2010 N 07AP- 1517/10).

Prepared answer:

Expert of the Legal Consulting Service GARANT

professional accountant Lazukova Ekaterina

Response quality control:

Reviewer of the Legal Consulting Service GARANT

Queen Elena

The material was prepared on the basis of an individual written consultation provided as part of the Legal Consulting service.

According to the Federal Law of 21.07.1997 N 122-FZ, rights to real estate and transactions with it are subject to state registration in the Unified State Register of Rights. According to paragraph 1 of Art. 14 of this Law, the state registration of the emergence and transfer of rights to real estate is certified by a certificate of state registration of rights. The form of the certificate and a special inscription are established by the Rules for maintaining the Unified State Register of Rights (clause 2 of article 14 of the above-mentioned Law).

The procedure for registration of records on the termination of rights, restrictions (encumbrances) is established in section. VI and Appendix N 12 of the Rules for maintaining the Unified State Register of Rights, approved by the Decree of the Government of the Russian Federation of 18.02.1998 N 219 (as amended and supplemented).

Since the entries in the Unified State Register of Rights must fully comply with the entries in the documents, including the certificate of state registration of rights, the use of the "Terminated" and "Canceled" stamps on the forms of certificates of state registration of rights upon termination of rights due to the transfer of ownership is permissible and does not contradict the established procedure for registering property rights to real estate.

V.P. Kolody

Tax Service Counselor of the Russian Federation

III rank

27.06.2005

alienation

Do I need it before 06/01/2014. put the stamp "Received" in cash receipts, and "Issued" on cash receipts? And what is the order - after 06/01/2014.?

But the cashier's stamp is not needed at all on the expense documents, since the Regulation No. 373-P does not require this.

From 01.06.2014, the instructions of the Bank of Russia dated March 11, 2014 No. 3210-U are in effect. Clause 4.4, clause 5.1 of Instruction No. 3210-U). That is, the cashier may be issued a stamp, the details of which at the level of a normative act are not unambiguously defined. It can be either the “Paid” stamp or the “Received” stamp.

As for the RSC, then, as in the first case, the affixing of a stamp (seal) on the document is not provided for by the Instructions. Therefore, the stamp is not stamped in the consumable.

The rationale for this position is given below in the materials of the Glavbuh System

Receipt cash order

When receiving money at the cash desk, you need to issue a cash receipt voucher in the form No. KO-1 (). This document is executed in one copy.

The form of the incoming cash order consists of two parts: directly the incoming cash order and the detachable part - the receipt. Give the receipt to the person who deposited the money.

Specify the content of the business transaction in the receipt note and the receipt for it on the "Basis" line. For example, "payment under contract No. 123 dated September 12, 2014". In the line “Including”, indicate the amount of VAT in figures or write “Without VAT”. In the line "Attachment" list the documents attached to the cash receipt order.

Receipt cash order must be signed by the chief accountant or accountant, and in their absence - by the head of the organization (entrepreneur), cashier. On the basis of the administrative document, the obligation to sign cash documents for the accountant may be assigned to another employee of the organization. The candidacy of an authorized employee is agreed with the chief accountant (if any). If the manager (entrepreneur) conducts cash transactions and draws up the documents personally, then the cash documents are signed by him.

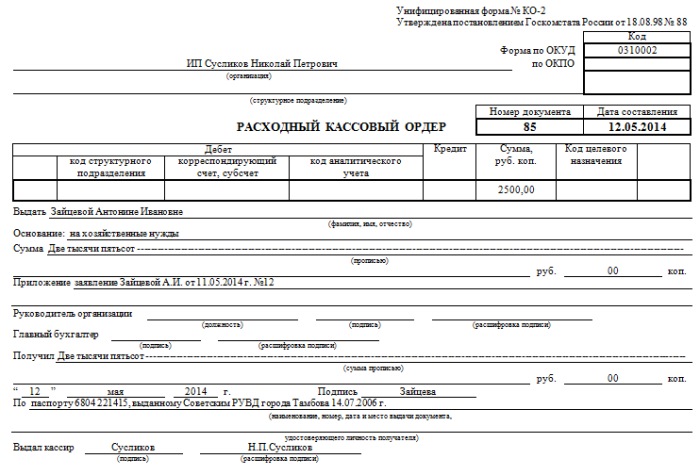

Account cash warrant

Issue money from the cash desk, issue an expense cash order according to the form No. KO-2 (). This document is drawn up in one copy.

If the money is issued to the employee on account of the report, then draw up the cash outflow order on the basis of his written application, drawn up in any form. Accept the application only if it is signed by the manager and it contains a record:

- on the amount of cash issued on account;

- about the period for which cash is issued;

- manager's signature;

- date.

Corrections in cash documents cannot be made (clause 4.7 of the instructions of the Bank of Russia dated March 11, 2014 No. 3210-U).

| The documents | Do I need a seal | Base |

| Financial documents | ||

| Documents for the accounting of cash transactions |

Mandatory: - on the last page of the cash book (Resolution of the Goskomstat of Russia dated August 18, 1998 No. 88, Methodological guidelines, approved); - on a receipt for an incoming cash order (form KO-1), which is transferred to the depositor (paragraph 5, clause 5.1 of the instructions of the Bank of Russia dated March 11, 2014 No. 3210-U); - in the payroll (form T-49), payroll (form T-53) - if the entry "deposited" is not made in front of the names and initials of employees who were not given money (paragraph 3, clause 6.5 of the instructions of the Bank of Russia dated March 11, 2014 No. 3210-U) |

Unified forms of primary accounting documentation for accounting of cash transactions, approved by resolutions of the Goskomstat of Russia dated August 18, 1998 No. 88, dated January 5, 2004 No. 1, by order of the Ministry of Finance of Russia dated December 15, 2010 No. 173n |

| Optional: on all other documents. In particular, on an expense cash order (form KO-2) * and in the accounting book of funds received and issued by the cashier (form KO-5) | ||

Situation:How to correctly put a seal (stamp) on a cash receipt order. The answer to this question depends on who the buyer of the goods is.

Place a seal in the part of the letterhead marked with the letters "M.P.", so that its imprint is located on the receipt.

The form of the incoming cash order consists of two parts: directly the incoming cash order and the detachable part - the receipt. There are no special rules for the location of the seal imprint (for example, 60% of the imprint on a receipt, and 40% on a receipt note) in the legislation. Therefore, put a seal in the part of the form marked with the letters "MP". Considering that this property is located on the receipt, the seal must be on it. This conclusion can be made on the basis of the decree of the State Statistics Committee of Russia dated August 18, 1998 No. 88.

The composition of the details that must be placed on the seal (stamp) of the cashier is also not established. Previously, normative acts were adopted that regulated this issue, but now they have been canceled (see, for example, the order of the Mayor of Moscow No. 843-RM dated August 25, 1998). Clause 6 of this document establishes a list of details that were previously mandatory:

- the full name of the organization in Russian with an indication of the organizational and legal form;

- location;

- main state registration number.

Now this list has been canceled (Moscow government decree of February 8, 2005 No. 65-PP), but it is advisable to publish this information in print. Usually the cashier uses not the main seal of the organization, but the seal for documents or cash register. Therefore, such seals make the appropriate inscription "For documents", "Cash desk" or "For cash documents", etc. (Clause 6.2 of the order of the Mayor of Moscow dated August 25, 1998 No. 843-RM).

Elena Popova

Article:Stamps on primary documents

In what cases is the stamp “Redeemed” put on the primary accounting documents?

Such a stamp can be used when registering cash transactions.

The procedure for conducting cash transactions by legal entities is regulated by Bank of Russia Ordinance No. 3210-U dated March 11, 2014. Clause 4.4 of Instructions No. 3210-U stipulates that the cashier is supplied with a seal or stamp that contains the details confirming the cash transaction. So, when accepting money, the cashier signs an incoming cash order, affixes an imprint of a seal (stamp) on the receipt to it and issues this receipt to the cash depositor (clause 5.1 of Direction No. 3210-U).

Thus, the cashier can be issued a stamp, the details of which are not uniquely determined at the level of a normative act.

In my opinion, it can be either the “Paid” stamp or the “Redeemed” stamp.

The reference to the stamp "Canceled" is contained in clause 4.5 of the Standard Rules for the Operation of Cash Register Machines in the Implementation of Cash Payments with the Population, approved by the Ministry of Finance of Russia on August 30, 1993 No. 104 (applied in the part that does not contradict the Federal Law of May 22, 2003 No. 54-FZ). At the same time, from the text of clause 4.3 of the Standard Rules, it can be concluded that such a stamp is affixed on unused cashier's checks.

Article:Registration of an incoming cash order

How to properly draw up a PKO: whether to put a seal on it, cut off or not a receipt for this document

Neither Instructions on filling out the PQS form, approved by the Resolution of the State Statistics Committee of Russia dated August 18, 1998, No. 88, nor the Regulation on the procedure for conducting cash transactions with banknotes and coins of the Bank of Russia on the territory of the Russian Federation, approved by the Central Bank of the Russian Federation October 12, 2011 No. 373-P.

In accordance with these documents, the cashier's stamp is sufficient for the PKO.

However, in reality, the absence of a round seal can lead to disputes, as evidenced by arbitration practice, for example, the resolution of the FAS of the East Siberian District of January 22, 2009 No. A33-11360 / 07-F02-7117 / 08.

Therefore, many organizations prefer that receipts to the PKO be certified with a round stamp. Then next to it you need to put the cashier's stamp "Paid" or "Accepted".

The receipt must be torn off and transferred to the one who brings the proceeds from the cash register to the organization's cash desk. This can be a senior cashier, a cashier-operator or another person who implements tourist services (clause 3.2 of the Regulations on the procedure for conducting cash transactions).

The person who donates money to the cashier keeps the receipt as proof that he has handed over all the proceeds.

How to correctly draw up cash receipts and receipts?

In the Procedurecash transactionsv Russian Federation it is indicated that cash receipts and cash receipts or documents replacing them immediately after receiving or issuing money on them are signed by the cashier, and the documents attached to them are canceled with a stamp or the inscription "Paid" indicating the date (date, month, year). The bank told us that the stamp “Redeemed” is stamped on expense orders, “Paid” on payrolls, and “Received” on receipts.

Is it so? Is it possible to put the stamp “Redeemed” on all documents? If it is necessary to put a stamp on the attached documents, is it necessary to put a stamp on separate expense orders, for example, for the issuance of money against a report? Our organization is located on the simplified tax system.

Procedure for maintaining cash transactions in the Russian Federation was approved in accordance with the Law of the Russian Federation of September 25, 1992, No. 3537-1 "On monetary system Russian Federation".

According to Art. 15 of this Law, the Bank of Russia (Central Bank of the Russian Federation) was entrusted with determining the procedure for maintaining cash transactions.

Currently, this Law is not in effect, but a similar provision is contained in Art. 34 of the Federal Law of the Russian Federation of July 10, 2002, No. 86-FZ "On Central Bank Russian Federation (Bank of Russia) ": for the purpose of organizing cash on the territory of the Russian Federation money circulation the Bank of Russia is responsible for determining the procedure for maintainingcash transactions .

In accordance with paragraphs 13, 14 of the Procedure cash transactions cash is accepted by the cash desks of enterprises on incoming cash orders, signed by the chief accountant or by a person authorized in writing by the head of the enterprise.

Acceptance of money is issued cash receipt receiptsigned by the chief accountant or a person authorized to do so and the cashier, certified by the seal (stamp) of the cashier or a print from a cash register.

Cash withdrawal from cash registers of enterprises produced or properly executed other documents(payroll (settlement and payment), applications for the issuance of money, accounts, etc.) with imposition stamp on these documents with the details of the cash outflow order. Documents for issuing money must be signed by the head, chief accountant of the enterprise or by persons authorized to do so.

Remuneration of labor, payment of benefits for social insurance and the scholarship is made by the cashier on payroll (settlement and payment) statements without drawing up an expense cash order for each recipient.

On the title (title) page of the payment (settlement and payment) statement, an authorization inscription is made for the issuance of money, signed by the head and chief accountant of the enterprise or persons authorized to do so.

In a similar manner, one-time issuance of money for labor remuneration (when going on vacation, illness, etc.) can be issued, as well as the issuance of deposited amounts and money under the report for expenses related to business trips, to several persons.

One-time payments of money for wages to individuals are made, as a rule, on cash outflow orders(clause 17 of the Procedure for maintaining cash transactions).

According to clause 20 of the Procedure cash transactions cash receipts and receipts or replacing documents immediately after receiving or issuing money on them, they are signed by the cashier, and the documents attached to them are redeemed with a stamp or the inscription "Paid" indicating the date (day, month, year).

Thus, incoming and outgoing cash orders are signed by the cashier, it is not necessary to put the “Paid” stamp on them.

On documents attached to cash receipts and receipts(statements, invoices, powers of attorney for the issuance of money, receipts for receipts, etc.), the stamp "Paid" is mandatory.

In practice, organizations put the stamp "Paid" both on the documents attached to cash orders and on the cash orders themselves, which is not a violation, since the Procedure for maintaining cash transactions does not contain a ban on cancellation of incoming and outgoing cash orders with the stamp "Paid".

The bank that gave you explanations could be guided by clause 2.21 of the Regulations on documents and workflow in accounting, approved by the Ministry of Finance of the USSR dated July 27, 1983, No. 105, according to which all documents attached to cash receipts and receipts, as well as documents that served basis for accrual wages, are subject to mandatory cancellation with a stamp or handwritten inscription "Received" or "Paid" with the date (day, month, year).

But, as already noted, the function of determining the order of cash transactions assigned to the Central Bank of the Russian Federation, therefore, the procedure for maintaining cash transactions in the Russian Federation, and not a document of the USSR Ministry of Finance.

Want to know more? ..

According to the legislation of the Russian Federation, enterprises and organizations are required to keep accounting records of all business transactions... To solve this problem, primary documents are used. Confirmation of the fact of transactions with cash at the cash register of the enterprise is also carried out using primary documents.

Consider the main types of cash documents (hereinafter CA) and what mandatory details they can and should contain.

Types depending on the nature of operations:

- incoming;

- expendable;

- accounting registers containing registration and generalized information from the primary CA listed above.

At the legislative level (Resolution of the Comstat of the Russian Federation No. 88), the following types of design documentation have been approved:

- cash receipt order - No. KO1 (hereinafter referred to as PKO);

- cash outflow order - No. KO2 (RKO);

- cash book - No. KO4 (KK);

- register of incoming and outgoing cash documents - No. KO3 (ZhR);

- accounting book of funds received and issued by the cashier - No. KO5 (KVD).

Highlight the main mandatory details of the documents listed above, namely:

Highlight the main mandatory details of the documents listed above, namely:

- title;

- date of its compilation;

- the name of its originator, in other words, the name of the organization / enterprise;

- Contents of operation;

- quantitative and monetary measurements of the transaction;

- the position of the persons who committed and issued;

- signatures of the persons mentioned above.

Basic requirements for registration

Due to the fact that the approved and the above-mentioned design documents differ from each other, consider the rules for the design of each.

Features of the design of the PKO:

- the essence of the operation is entered in the line "Base";

- the total amount of VAT is entered in the line "Incl." numerically. This line cannot be empty. If the tax is not applied, the phrase “without (VAT)” should be entered;

- data on additional supporting documents (if any) are entered in the PKO in the line "Appendix".

When filling out a cash register, it is necessary to take into account the following nuances:

- the presence of additional documents (for example, a power of attorney) is entered in the "Appendix" line with the obligatory indication of the date and number;

- the line "Basis" implies the reflection of the content of the expense transaction;

- the presence of the manager's signature is optional if it is present on the attached document. For example, if the signature of the director of the enterprise is present on the order together with the resolution "Allow" or "Approved", then the cash settlement can be accepted into work without his signature.

Separately, we will consider the issue of requirements for affixing stamps on RKO and PKO. According to the Decree of the Central Bank of the Russian Federation No. 3210-U dated 03/11/14 on conducting cash transactions, the mandatory requirements for stamp imprinting are not stipulated, as was the case before 2014. Previously, the stamps “Paid” were used on the receipt note and “Redeemed” on the expense note. The current rules imply only the obligatory affixing of a stamp on the tear-off receipt to the PKO. Thus, the stamp "Paid" can be affixed to the receipts to the PKO. The presence of an imprint "Paid" is a confirmation of the actual deposit of money and their posting.

As for the stamp "Redeemed":

- it is put down on the sheets, for example, when salaries are issued to employees;

- can be used instead of "Paid", for example, if the stamp is lost or missing for another reason.

There are 3 basic rules on how to issue a QC:

- Flash.

- Number. Essence: each sheet is numbered (sequential serial number).

- Seal. Essence: it is necessary to indicate how many sheets are contained in the QC according to the assigned numbering and to certify this inscription. This inscription is placed at the end of the book and is considered certified if there is a signature of the director and chief accountant.

The QC form assumes the presence of 2 parts. Moreover, the second part is tear-off. It serves as a cashier's report at the end of the day and can only be torn off after the end of all transactions.

The name itself answers the question of what this form is intended for, namely the assignment of serial registration numbers to cash documents.

Assumes filling in such information:

- PKO / RKO No., date and amount in Russian rubles numerically;

- columns "Note" are filled in if necessary.

Filling in the KVD is justified if there are several cashiers on the staff of the organization, including the senior one.

Features of the design of the KVD:

- the amount transferred by the senior cashier to the subordinate employee is reflected in the line “Issued” or “Handed over”;

- the signatures of both persons must be affixed in the lines “Money received”.

What are the mandatory rules and requirements that must be followed when registering primary design documents:

- Affixing the signatures of the chief accountant and the cashier is mandatory.

- Mandatory presence of a stamp on the tear-off receipt - "Paid".

- The seal (stamp) is not affixed to the cash settlement, but the presence of the recipient's signature is mandatory.

- The design of the CD can be both on paper and in electronic form.

- The electronic version of the document is drawn up using special. technology (computer, printer).

- The paper version is filled by hand with a ballpoint pen, ink or using a typewriter.

- Blank lines that do not contain information are marked with a dash.

The chief accountant is the person in charge in the issue of drawing up the CD. In his absence, the manager becomes the person responsible for the preparation of cash documents, which is carried out under his control.

Fixes in CD

The main rule or requirement for CA that should be highlighted is the absence of corrections in the accounting registers.

CD should not contain corrections, blots. In practice, performers make edits to the document using correction fluids. Such actions are not allowed.

Consider the main options for how corrections can be made to cash documents:

- The mistake was made in PKO or RKO.

It is forbidden to make corrections in any way (manually, strikethrough, smearing). The only solution in this case would be to cross out the PKO / RKO with errors and draw up a new one. The damaged (crossed out) order is added to the cashier's report for the day. It is prohibited to carry out an operation of spending or accepting money on the basis of a damaged document.

- An error has been made in the Journals or Cash Book.

It is forbidden to use correction fluid, cleanup.

Corrections are allowed as follows:

- the incorrectly entered inscription is crossed out so that the erroneous inscription can then be read;

- corrections are made above the crossed out inscription by prescribing the correct amount or text;

- next to the corrected or in the free fields of the document, the inscription is affixed: "Corrected" and must be signed by all persons responsible for maintaining and forming the CA;

- signatures are decrypted, and the date of the amendment is indicated;

- corrections are made to all copies.

CD storage

The head organizes and implements the process, determines the storage locations and approves the procedure for the formation and storage of cash documents in the organization. He must ensure such storage conditions that the documents are safe throughout the period established by law.

General requirements in terms of shelf life are established in the Federal Law “On Bukh. accounting ", according to which, primary documents and registers of CA are stored in the archive for at least 5 years. After the expiration of the established period, they can be destroyed, but provided that there are no disputes on them, there are no ongoing legal proceedings.

It should be noted that the period of 5 years is counted from the date not of the creation of the document, but from the date of the reporting year in which they were formed.

Storage can be organized both in the archive at the enterprise and with the involvement of specialized firms. They hold contractual and fee-based storage for as many years as you need.

The above-mentioned law establishes that when conducting cash transactions in electronic form, the storage period for electronic media must also be the same as for paper media - not less than 5 years. An exception is the payroll for which employees are paid. They are stored for 75 years.

Storage of CD should be carried out on the basis of the following rules:

- Documents must be stapled in the context of each day. The deadline for the formation of the stitching is not later than the next working day.

- Inside the stitching, CDs must be selected according to the following order: in ascending order of account numbers. In the sequence, first of all by Dt account, and then by CT.

- All stitching sheets are subject to numbering.

- When transferring to the archive, an inventory is formed indicating the number and name of the CD stitching, an article can be affixed according to the nomenclature approved by the organization.