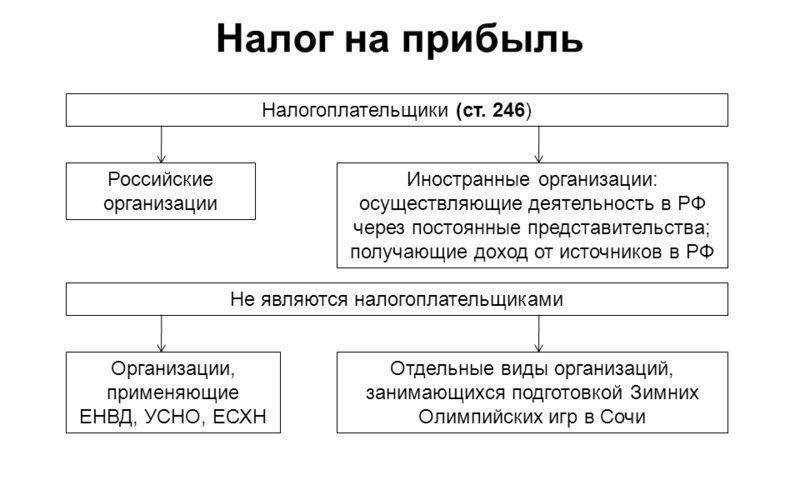

It is an important calculation criterion when determining the financial stability of a company. This metric explains how much money a company makes after deducting all possible expenses and also determines the success of the business.

The higher it is, the better, because for example, if you compare enterprises with approximately the same gross income, then the one that can boast of a higher income will be more successful. And this is an important wake-up call for both partners and potential investors. It is important for every business owner to know in detail how to calculate the net profit of an enterprise. This way he will be able to optimize its operation, as well as find possible weak points.

Dear readers! Our articles talk about typical ways to resolve legal issues, but each case is unique.

If you want to know how to solve exactly your problem - contact the online consultant form on the left or call

8 (499) 350-44-96

It's fast and free!

The difference between net profit and total

The term “net profit” means the amount that remains after all expenses have been subtracted from revenue. In economics, it is divided into several types. For example, net profit or NetProfit (hereinafter NP) is capital that completely belongs to the business owner.

The latter has the right to use it at his own discretion - cash it, invest in production, replenish working capital, etc. Its main difference from the general one is that the first is the final amount remaining after all possible costs have been discarded, and the second is calculated without taxes. Depending on the type, profit is calculated using different formulas.

Total profit refers to the amount remaining after deducting all costs from what was earned. How is a company's profit calculated? If you follow the formulas generally accepted in the West, this indicator is determined very simply. The formula for total profit looks like this:

(P) = TR – VAT – PC – ET, where

- TR—total revenue;

- VAT - value added tax;

- PC - cost;

- ET - excise taxes.

Profit before tax

In this case, a financial indicator is considered that reflects the positive results of the company. The presence of income means that commercial activities are carried out successfully, and the company operates efficiently and fulfills its tasks.

Profitability or unprofitability in the economy is determined very simply - by comparing income and expenses for the reporting period. The latter include:

- employees' salary;

- costs of consumables, components, etc.;

- marketing;

- public utilities;

- payment of rent;

- associated costs.

Note: if income exceeds expenses, then the organization is considered profitable; if, on the contrary, it is unprofitable.

The formula for calculating earnings before taxes (EBT) is as follows:

EBT = SR + OrI + OtI – OrE – OtE, where

- SR - sales receipts;

- OrI - ordinary income;

- OtI - other income;

- OrE - ordinary costs;

- OtE - other expenses.

Net profit

This indicator refers to the funds that remain after all possible expenses, fees, payments, taxes and all kinds of deductions have been subtracted. They belong entirely to the business owner and can be used by him for personal purposes or for further investment. Their size depends on factors such as:

- cost of goods/services;

- companies;

- taxes;

- additional expenses.

- Calculation formula No. 1: NP = TR – PC – *T – (OrE + OtE);

- Formula No. 2: NP = *FP + *GP + *OP – T;

- Formula No. 3: NP = EBT – T.

Note: There is also such a thing as net income. Although they are often confused, in fact they are not identical, i.e. NP is not net income (the calculation formula in this case is different). In simple terms, net income is revenue minus all expenses, and NP is net income minus all possible taxes and deductions.

Calculation of net profit on the balance sheet

Tax reporting is an indispensable condition for the operation of any commercial enterprise. To figure out how much to pay the state, accounting relies on BFP (). It is completely identical to EBT. Making errors in calculations is fraught with a decrease in NP and general losses.

The formula for calculating the net profit of an enterprise on the balance sheet was adopted to standardize the process. This in turn makes it as simple, transparent and convenient as possible. For this purpose, codes are used for their document called “Income Statement”.

An example of calculating enterprise profit

In this case, the entire process is standardized for greater convenience, and the calculation looks like this:

page 2400 = page 2110 + page 2340 – (page 2120 + page 2210 + page 2220) – page 2350 – page 2410

- line 2400 - net profit;

- line 2110 - revenue;

- line 2120 + line 2210 + line 2220 - cost + standard expenses;

- line 2340 - other income;

- line 2350 - other expenses;

- page 2410 - income tax.

Using the example above, you can learn how to correctly calculate the profit of an organization. So, there is a certain company for which you need to display NP for 2016. Respectively:

- indicators - TR (total revenue), PC (cost), CE (commercial expenses), MC (administrative expenses), OtI (other income), OtE (other expenses), T (income tax);

- code - 2110, 2120, 2210, 2220, 2340, 2350, 2410;

- period (2016) - 150000, 40000, 10000, 15000, 5000, 2000, 11500.

Note: after applying the formula (here it is presented in the European format, but using the domestic accounting form you can easily substitute the necessary concepts), the following equation is obtained: 150000 + 5000 – (40000 + 10000 + 15000) – 2000 – 11500 = 76500. The final amount will be that the most sought-after quantity.

Why is this formula so important? This indicator best demonstrates the success of the company. Potential investors, managers and shareholders will always first of all look at the dynamics of growth of the company's net earnings. After all, it is obvious that the higher the net income, the better for the business. Although this also has its own nuances. The fact that a company has high net income in a particular period of time does not mean that it will demonstrate stable growth in the future.

Revenue from sales

Earnings from sales are the most important evaluation criterion for determining the efficiency of a commercial structure. It indicates whether the company has managed to achieve profitability and whether it is worth continuing to operate in the future. Having complete control over costs and expenses is essential.

In addition, this coefficient is applicable not only to assess the overall performance of the company, but also to compare two competitive enterprises(although in the latter case this is not always effective). To calculate revenues from the sale of goods and services, a simple formula is used.

SR = GP – MC – CE, where

- GP - ;

- MC - management expenses;

- CE - commercial expenses.

Formula Vpr (gross profit):

GP = TR – PC, where

- TR - total revenue;

- PC is the cost of goods sold.

Correct accounting of a company’s profitability indicators will allow an objective assessment of its capabilities and prospects

Every entrepreneur needs to strive to ensure that the profitability indicator reaches, if not maximum values, then at least simply positive ones. If its total value is not enough to cover costs, the business is doomed to failure. It should be noted that sales revenues alone for a specific period do not say anything about the success of the company. An accurate assessment can be obtained only after comparing these data with other indicators for a similar period of time, as well as by tracking the overall dynamics of their changes.

So, to obtain an objective picture of the economic situation at the enterprise, it is necessary to consistently study all indicators month after month. If the trend is positive, it is a sign that the business is expanding at a steady pace and growth can be expected in the future. So, entrepreneurs who want to attract outside investment into their company need to try to ensure that comparative accounting data is only “positive” for at least one year.